OTC Markets Listing Requirements 2026

OTC Markets Listing Requirements 2026: How to List on OTCQX, OTCQB or OTCID Companies seeking an OTC Markets quotation in 2026 must…

Read MoreBlog

Insights on securities law, exchange listings, going public, SEC reporting, and market regulation. Stay updated with our latest articles on capital markets compliance, regulatory developments, and strategic guidance for public and private companies.

OTC Markets Listing Requirements 2026: How to List on OTCQX, OTCQB or OTCID Companies seeking an OTC Markets quotation in 2026 must…

Read MoreOn August 5, 2026, the Securities and Exchange Commission announced the creation of a specialized Financial Reporting and Accounting Unit within its…

Read MoreThe July 22, 2026 order approving Nasdaq’s new $5 million Market Value of Listed Securities continued-listing standard has been automatically stayed after…

Read MoreShort selling is a lawful and valuable component of market efficiency. It provides liquidity, supports price discovery, and uncovers fraud. But when…

Read MoreNasdaq Uplisting Requirements, Undisclosed Lockups, Manufactured Public Float, Matched Trading and Misleading Listing Applications An uplisting from the OTC Markets to the…

Read MoreNasdaq-listed companies now face an additional and potentially unforgiving continued listing requirement. Under the SEC-approved rule, a company whose Market Value of…

Read MoreThe Securities and Exchange Commission has approved a new Nasdaq continued listing requirement that may lead to the rapid suspension and delisting…

Read MoreThe first contentious proceedings ever brought against the International Seabed Authority have placed the rights of deep-sea mining contractors, the limits of…

Read MoreBOEM Moves Toward a Historic Seabed Minerals Lease Sale The Bureau of Ocean Energy Management has taken a significant step toward holding…

Read MoreAn SEC-reporting company placed on the OTC Markets Expert Market ordinarily has two distinct problems. First, it must cure its delinquent reporting…

Read MoreLawmakers seek ticker warnings and 10-business-day trading suspensions, but a temporary SEC suspension can become a practical death sentence for a stock.…

Read MoreThe Securities and Exchange Commission is considering a FINRA proposal that would significantly modernize the public reporting of short interest in U.S.…

Read MoreUpdated July 15, 2026 | SEC trading suspensions, Nasdaq microcap fraud, WhatsApp stock scams When the Securities and Exchange Commission suspended trading…

Read MoreNew SEC guidance increases transparency in shareholder activism and proxy contests By Brenda Hamilton, Securities and Going Public Lawyer | Current through…

Read MoreForeign companies frequently want access to U.S. investors without the time, cost and regulatory burden of becoming full SEC reporting companies. For…

Read MoreA comprehensive guide to OTCQX International eligibility, quotation, Rule 15c2-11, Form 211 and ongoing compliance under the April 6, 2026 V11 rules Current through…

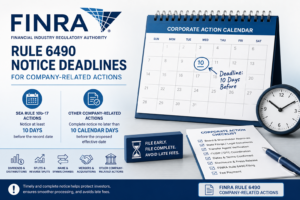

Read MoreSubmission status is only the beginning After a company-related action request is submitted, FINRA may assign a case number or provide electronic…

Read MoreFee categories under Rule 6490 FINRA Rule 6490 identifies specific fees for processing certain corporate action notifications and related requests. The most…

Read MoreOnce a company decides to go public, what it says — and where, when, and to whom it says it — comes…

Read MoreQuick answer: what can an issuer say during the IPO quiet period? An issuer can usually continue factual, ordinary-course business communications during…

Read MoreA Practical Guide for Issuers, Boards, Counsel, Transfer Agents and Practitioners Under Amended Nasdaq Rule 5250(e)(7) Current through June 18, 2026. Nasdaq-listed…

Read MoreNasdaq listing analysis often begins with financial standards, bid price, public float, shareholder counts and corporate governance. But those standards cannot be…

Read MoreInternal approval is not the same as a FINRA notice An issuer is generally considered to have provided notification when it submits…

Read MoreManagement’s Discussion and Analysis of Financial Condition and Results of Operations, commonly referred to as MD&A or MDA, is one of the…

Read MoreA Form S-1 registration statement is the central disclosure document used by many companies that want to register securities with the Securities…

Read MoreThe deadline depends on the action FINRA Rule 6490 separates actions into two broad categories. The first category is an SEA Rule…

Read MoreStart with the official rule text Issuers looking for information about FINRA Rule 6490 should begin with the current text of FINRA…

Read MoreWhy Nasdaq compliance matters A Nasdaq listing can be a major milestone for a public company. It can increase market visibility, broaden…

Read MoreWhy Rule 6490 Matters FINRA Rule 6490 is one of the most important rules for public companies whose securities trade over…

Read MoreMarketing an initial public offering is not the same as marketing an ordinary product launch. In a U.S.-registered IPO, every communication about…

Read MoreExplore our curated collection of external resources and industry links that complement our blog content. These hand-picked links provide additional perspectives on securities law, market regulations, and business compliance.